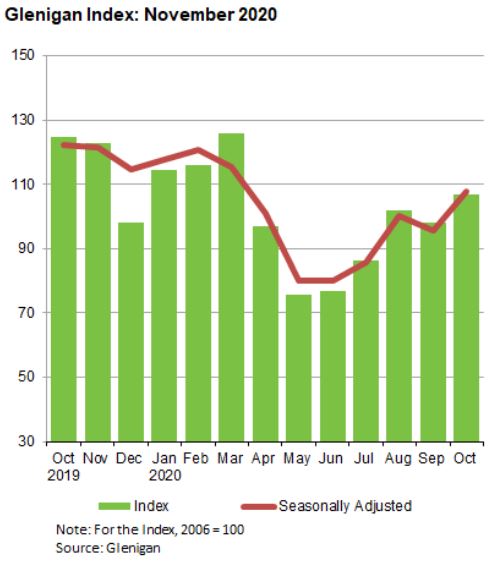

Recovery in project-starts continues

– The value of underlying work (under £100 million) starting on-site during the three months to October was 14% lower than a year ago, however increased by 26% compared to the preceding three months on a seasonally adjusted basis.

– Residential starts declined 16% against the previous year but increased 35% on the preceding three months.

– Non-residential work commencing on-site climbed 10% on the preceding three months but declined by a fifth compared to the previous year.

– Civil engineering experienced a strong three months, rising 22% on the previous year and 52% against the preceding three months.

The three months to October marked a strong recovery in the value of work starting on-site in all sectors and regions against the lows of the previous three month period. The value of construction work starting on-site in October alone was almost double that of May.

Project-starts are still heavily below pre-pandemic levels, but the gap is narrowing. The value of work commencing on-site in October was 14% lower than a year ago, whereas in May construction-starts were 46% lower. However, with the winter period now approaching, Britain’s relationship with the European Union still uncertain and with the initial backlog of delayed project-starts now cleared, we anticipate growth to be slow over the coming months through to 2021.

Non-residential projects commencing on-site declined by 20% compared to a year ago, but climbed 10% on the preceding three months (seasonally adjusted).

The health sector experienced the biggest rise in the value of project-starts against the previous year, rising 30%. Starts also increased 37% against the preceding three months.

Office starts during the three months to October climbed 6% against the previous year and 47% compared to the preceding three months.

The value of hotel & leisure project-starts experienced the sharpest fall of any sector, declining 54% compared to a year ago. Work commencing on-site also declined by a quarter against the preceding three months.

Education starts also suffered steep declines of 32% against the previous year and 17% compared to the preceding three months.”

The civil engineering sector experienced an exceptional three months to October, with the value of work starting on-site increasing 22% on the previous year and 52% on the preceding three months on a seasonally adjusted basis.

The value of utilities project-starts experienced the greatest rise against the preceding three months of any sector, rising 122%. Starts also climbed 8% compared to a year ago.

Infrastructure work commencing on-site increased 30% on the previous year and 28% on the preceding three months.

UK Regions start to return to growth

The value of project-starts in most UK regions were still lower than a year ago. However, a few regions achieved growth for the first time since the national lockdown began in March.

Construction-starts in Wales experienced the greatest rise with an increase of 24% compared to a year ago. Against the preceding three months (seasonally adjusted) starts climbed 12%.

The West Midlands and South West also had a relatively good three months to October, with the value of starts rising 7% and remaining unchanged on the previous year respectively. Work commencing on-site increased by 55% in the West Midlands and 52% in the South West compared to the preceding three months.

Despite a fall in the value of project-starts of 15% on the previous year, Scotland experienced the sharpest growth against the preceding three month period with a rise of 74%.

Work starting on-site in the East Midlands during the three months to October declined 38% against the previous year; the heaviest fall of any region. Starts fell 27% in both the East of England and North West.

The East Midlands, South East and North East were the only three regions to experience declines in the value of project-starts compared to the preceding three months, with falls of 2%, 6% and 8% respectively.

Glenigan Indices (underlying* projects up to £100 million)

|

|

Glenigan Index |

Residential |

Non-residential |

Civil engineering |

||||

|

|

Index |

% Change |

Index |

% Change |

Index |

% Change |

Index |

% Change |

|

Oct-19 |

124.7 |

-12% |

153 |

-11% |

110 |

-18% |

101 |

30% |

|

Nov-19 |

122.7 |

-14% |

140 |

-17% |

111 |

-16% |

122 |

18% |

|

Dec-19 |

98.0 |

-20% |

113 |

-25% |

89 |

-18% |

92 |

-3% |

|

Jan-20 |

114.4 |

-13% |

130 |

-19% |

104 |

-5% |

113 |

-19% |

|

Feb-20 |

116.1 |

-13% |

137 |

-16% |

103 |

-5% |

111 |

-28% |

|

Mar-20 |

125.7 |

-18% |

147 |

-16% |

107 |

-18% |

142 |

-26% |

|

Apr-20 |

97.0 |

-33% |

115 |

-34% |

77 |

-36% |

128 |

-17% |

|

May-20 |

75.5 |

-46% |

86 |

-50% |

57 |

-51% |

124 |

-13% |

|

Jun-20 |

76.7 |

-47% |

81 |

-56% |

66 |

-44% |

108 |

-16% |

|

Jul-20 |

86.3 |

-44% |

96 |

-50% |

78 |

-38% |

93 |

-38% |

|

Aug-20 |

101.7 |

-33% |

117 |

-41% |

93 |

-25% |

91 |

-32% |

|

Sep-20 |

98.0 |

-35% |

117 |

-40% |

82 |

-33% |

108 |

-19% |

|

Oct-20 |

106.8 |

-14% |

128 |

-16% |

88 |

-20% |

123 |

22% |